Why Abundance, Security, and Free Markets are the Only True Catalysts for Innovation

Introduction: The Paradox of Creation

In the modern economic narrative, competition is lionized as the engine of progress. We are taught that a fierce marketplace, where rivals battle for supremacy, drives innovation, lowers prices, and ultimately benefits society. However, a closer examination of the last three decades of technological advancement reveals a startling paradox: true, transformative innovation—the kind that leaps from zero to one—rarely emerges from the bloody trenches of perfect competition. This notion supports the idea that perfect competition stifles progress and creativity, leading us to question why abundance, security, and free markets are the only true catalysts for innovation, as these environments often look far more like a monopoly with long-term vision rather than a cutthroat market.

This thesis, most forcefully articulated by entrepreneur and investor Peter Thiel in his seminal work, Zero to One, argues that progress is not a product of incremental improvements in a crowded field, but of bold new creations that establish temporary monopolies [1]. This article will explore Thiel’s framework, arguing that the capacity for radical innovation is contingent upon the financial security and long-term planning horizons that only sustained profitability can provide.

We will then turn our lens to the European Union, particularly Germany, to diagnose why the continent has failed to produce world-dominating technology companies in recent decades, attributing this failure to a culture of short-termism, stifling regulation, and punitive taxation.

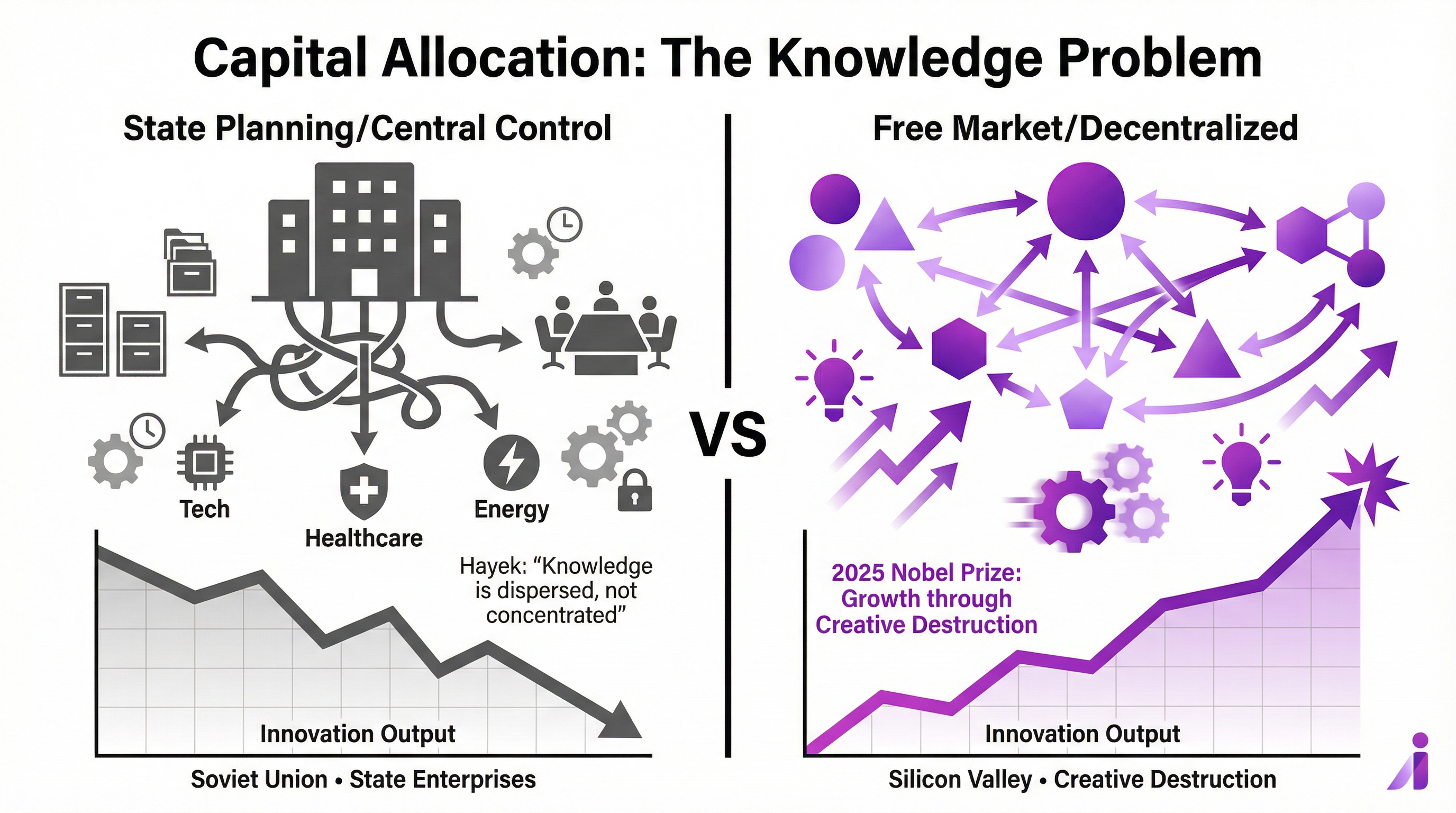

Finally, we will dismantle the notion that the state can act as an effective substitute for the market in allocating capital for innovation. Drawing on the work of Nobel Prize-winning economists like Friedrich Hayek and the laureates recognized for their work on creative destruction, we will demonstrate that centralized planning is, and has always been, the most inefficient allocator of resources, fundamentally at odds with the chaotic, decentralized, and often wasteful process that defines true invention.

The Thiel Doctrine: Competition is for Losers

Peter Thiel’s provocative assertion that “competition is for losers” is not an endorsement of anti-competitive practices but a fundamental critique of how we perceive value creation. He draws a sharp distinction between “0 to 1” innovation, which involves creating something entirely new, and “1 to n” innovation, which consists of copying or iterating on existing models. While globalization represents the latter, spreading existing technologies and ideas, true progress is defined by the former.

To understand this, Thiel contrasts two economic models: perfect competition and monopoly.

In a state of perfect competition, no company makes an economic profit in the long run. Firms are undifferentiated, selling at whatever price the market dictates. If there is money to be made, new firms enter, supply increases, prices fall, and the profit is competed away. In this brutal struggle for survival, companies are forced into a short-term, defensive crouch. Their focus is on marginal gains and cost-cutting, not on ambitious, long-term research and development projects that may not pay off for years, if ever [1].

The U.S. airline industry serves as a prime example. Despite creating immense value by transporting millions of passengers, the industry’s intense competition drives profits to near zero. In 2012, for instance, the average airfare was $178, yet the airlines made only 37 cents per passenger trip [1]. This leaves no room for the “waste” and “slack” necessary for bold experimentation.

In stark contrast, a company that achieves a monopoly—not through illegal means, but by creating a product or service so unique and superior that it has no close substitute—can generate sustained profits. These profits are not a sign of market failure but a reward for creating something new and valuable. Google, for example, established a monopoly in search in the early 2000s. Its resulting profitability allowed it to invest in ambitious “moonshot” projects like self-driving cars and artificial intelligence, endeavors that a company struggling for survival could never contemplate.

This environment of abundance and security is the fertile ground from which “Zero to One” innovations spring. It allows a company to think beyond immediate survival and plan for a decade or more into the future, accepting the necessity of financial

waste and the high probability of failure in the pursuit of groundbreaking discoveries. This is the core of the Thiel doctrine: progress requires the security that only a monopoly, however temporary, can provide.

The European Malaise: A Continent of Incrementalism

For the past three decades, a glaring question has haunted the economic landscape: where are Europe’s Googles, Amazons, or Apples? Despite a highly educated workforce, strong industrial base, and significant government investment in R&D, the European Union, and Germany in particular, has failed to produce a single technology company that dominates its global market. The continent’s tech scene is characterized by a plethora of “hidden champions”—highly successful, niche-focused SMEs—but it lacks the breakout, world-shaping giants that have defined the digital age. This is not an accident of history but a direct consequence of a political and economic culture that is fundamentally hostile to the principles of “Zero to One” innovation.

The Triple Constraint: Regulation, Taxation, and Short-Termism

The European innovation deficit can be attributed to a trifecta of self-imposed constraints:

- A Culture of Precautionary Regulation: The EU’s regulatory philosophy is governed by the “precautionary principle,” which prioritizes risk avoidance over seizing opportunities. This manifests in sprawling, complex regulations like the General Data Protection Regulation (GDPR) and the AI Act. While well-intentioned, these frameworks impose immense compliance burdens, especially on startups and smaller firms. A 2021 study found that GDPR led to a measurable decline in venture capital investment and reduced firm profitability and innovation output, as resources were diverted from R&D to legal and compliance departments [2]. The AI Act, with its risk-based categories and strict mandates, creates further bureaucratic hurdles that stifle the rapid, iterative experimentation necessary for AI development. This risk-averse environment encourages incremental improvements within established paradigms rather than the disruptive breakthroughs that challenge them.

- Punitive Taxation and the Demand for Premature Profitability: European tax policies, particularly in countries like Germany where the average corporate tax burden is around 30%, create a significant disadvantage for innovation-focused companies [3]. High taxes on corporate profits and wealth disincentivize the long-term, high-risk investments that drive transformative innovation. Furthermore, the European venture capital ecosystem is less developed and more risk-averse than its U.S. counterpart. Startups often rely on bank lending, which demands a clear and rapid path to profitability. This pressure to become profitable quickly is antithetical to the “wasteful” and often decade-long process of developing truly novel technologies. As a result, many of Europe’s most promising startups, such as UiPath and Dataiku, have relocated to the U.S. to access larger markets, deeper capital pools, and a more favorable regulatory environment [2].

- A Fragmented Market: Despite the ideal of a single market, the EU remains a patchwork of 27 different national laws and regulatory interpretations. This fragmentation prevents European companies from achieving the scale necessary to compete with their American and Chinese rivals. A startup in one member state may face entirely different compliance requirements in another, creating significant barriers to expansion. This stands in stark contrast to the unified markets of the U.S. and China, where companies can scale rapidly to achieve national and then global dominance.

This combination of overregulation, high taxation, and market fragmentation creates an environment where it is nearly impossible for companies to achieve the sustained profitability and security necessary for “Zero to One” innovation. The European model, in essence, enforces a state of perfect competition, trapping its companies in a cycle of incrementalism and ensuring that the next generation of technological giants will be born elsewhere.

The State as Innovator: A Proven Failure

Faced with this innovation deficit, some policymakers in Europe and elsewhere have been tempted by the siren song of industrial planning.

The argument is that the state, with its vast resources and ability to direct investment, can strategically guide innovation and pick winners. This is a dangerous and historically discredited idea. The 2025 Nobel Prize in Economics, awarded to Philippe Aghion, Peter Howitt, and Joel Mokyr for their work on innovation-led growth, serves as a powerful reminder that prosperity comes not from stability and central planning, but from the chaotic and unpredictable process of “creative destruction” [4].

The Knowledge Problem and the Price System

Nobel laureate Friedrich Hayek, in his seminal work, dismantled the socialist belief that a central authority could ever effectively direct an economy. He argued that the knowledge required for rational economic planning is not concentrated in a single mind or committee but is dispersed among millions of individuals, each with their own unique understanding of their particular circumstances. The market, through the price system, acts as a vast, decentralized information-processing mechanism, coordinating the actions of these individuals without any central direction [5].

As Hayek wrote, “The economic problem of society is thus not merely a problem of how to allocate ‘given’ resources—if ‘given’ is taken to mean given to a single mind which could solve the problem set by these ‘data.’ It is rather a problem of how to secure the best use of resources known to any of the members of society, for ends whose relative importance only these individuals know” [5].

State-led innovation initiatives inevitably fail because they are blind to this dispersed knowledge. A government committee, no matter how well-informed, cannot possibly possess the information necessary to make the millions of interconnected decisions required to bring a new technology to market. The historical record is littered with the failures of central planning, from the economic collapse of the Soviet Union to the stagnation of countless state-owned enterprises.

Creative Destruction: The Engine of Progress

The work of the 2025 Nobel laureates reinforces Hayek’s critique. Joel Mokyr’s historical analysis of the Industrial Revolution reveals that it was not the product of government programs but of a cultural shift towards open inquiry, merit-based debate, and the free exchange of ideas. The political fragmentation of Europe, which allowed innovators to flee repressive regimes, was a key factor in this process [4].

Aghion and Howitt’s model of “growth through creative destruction” shows that a dynamic economy depends on a constant process of experimentation, entry, and replacement. New, innovative firms challenge and displace established ones, driving progress. This process is inherently messy and unpredictable. It cannot be “engineered” or “guided” by a central planner. Attempts to protect incumbents or strategically direct innovation only serve to entrench mediocrity and stifle the very dynamism that drives growth.

Policies like Europe’s employment protection laws, which make it difficult and expensive to restructure or downsize a failing venture, work directly against this process. A dynamic economy requires that entrepreneurs be free to enter the market, fail, and try again without asking for the state’s permission or being cushioned from the consequences of failure.

The Market at Work: Three Stories of Innovation and Regulation

To make the abstract principles of market dynamics and regulatory friction concrete, consider three powerful stories of technologies that share common roots but followed radically different cost trajectories. These case studies vividly illustrate how free, competitive markets drive costs down and quality up, while regulated, third-party-payer systems often achieve the opposite.

Story 1: LASIK—A Clear View of the Free Market

LASIK eye surgery is a modern medical miracle, yet it operates almost entirely outside the conventional health insurance system. As an elective procedure, it is a cash-pay service where consumers act as true customers, shopping for the best value. The results are a textbook example of free-market success. In the late 1990s, the procedure cost around $2,000 per eye in today’s dollars. A quarter-century later, the price has not only failed to rise with medical inflation but has actually fallen in real terms, with the average cost remaining around $1,500-$2,500 per eye [6].

More importantly, the quality has soared. Today’s all-laser, topography-guided custom LASIK is orders of magnitude safer, more precise, and more effective than the original microkeratome blade-based procedures. This combination of falling prices and rising quality is what we expect from every other technology sector, from televisions to smartphones. It happens in LASIK for one simple reason: providers compete directly for customers who are spending their own money. There are no insurance middlemen, no complex billing codes, and no government price controls to distort the market. The result is relentless innovation and price discipline.

Story 2: The Genome Revolution—Faster Than Moore’s Law

The most stunning example of technology-driven cost reduction in human history is not in computing, but in genomics. When the Human Genome Project was completed in 2003, the cost to sequence a single human genome was nearly $100 million. By 2008, with the advent of next-generation sequencing, that cost had fallen to around $10 million. Then, something incredible happened. The cost began to plummet at a rate that far outpaced Moore’s Law, the famous benchmark for progress in computing. By 2014, the coveted “$1,000 genome” was a reality. Today, a human genome can be sequenced for as little as $200 [7].

This 99.9998% cost reduction occurred in a field driven by fierce technological competition between companies like Illumina, Pacific Biosciences, and Oxford Nanopore. It was a race to innovate, fueled by research and consumer demand, largely unencumbered by the regulatory thicket of the traditional medical device market. While the interpretation of genomic data for clinical diagnosis is regulated, the underlying technology of sequencing itself has been free to follow the logic of the market, delivering exponential gains at an ever-lower cost.

Story 3: The Insulin Tragedy—A Century of Regulatory Failure

In stark contrast to LASIK and genomics stands the story of insulin, a life-saving drug discovered over a century ago. The basic technology for producing insulin is well-established and inexpensive; a vial costs between $3 and $10 to manufacture. Yet, in the heavily regulated U.S. healthcare market, the price has become a national scandal. The list price of Humalog, a common insulin analog, skyrocketed from $21 a vial in 1996 to over $332 in 2019—a more than 1,500% increase [8].

How is this possible? The answer lies in a web of regulatory capture and market distortion. The U.S. patent system allows for “evergreening,” where minor tweaks to delivery devices or formulations extend monopolies. The FDA’s classification of insulin as a “biologic” has historically made it nearly impossible for cheaper generics to enter the market. Most critically, a shadowy ecosystem of Pharmacy Benefit Managers (PBMs) negotiates secret rebates with manufacturers, creating perverse incentives to favor high-list-price drugs. The FTC even sued several PBMs in 2024 for artificially inflating insulin prices [9]. In this system, the consumer is not the customer; the PBM is. The result is a market where a century-old, life-saving technology has become a luxury good, a tragic testament to the failure of a market that is anything but free.

These three stories—of sight, of self-knowledge, and of survival—tell a single, coherent tale. Where markets are free, transparent, and competitive, innovation flourishes and costs fall. Where they are burdened by regulation, obscured by middlemen, and captured by entrenched interests, the consumer pays the price, both literally and figuratively.

Conclusion: Embracing the Monopoly of Progress

The evidence is clear we have a conundrum: true, transformative innovation is not a product of competition alone but in its’ results – not in ensuring same suboptimal outcome by regulated process. It requires an environment of abundance and security where companies can afford to think long-term, embrace risk, and invest in the “wasteful” process of discovery. Peter Thiel’s framework, far from being a defense of predatory monopolies, is a call to recognize the conditions necessary for human progress.

The failure of the EU and Germany to produce world-leading technology companies is a direct result of their hostility to these conditions. A culture of precautionary regulation, punitive taxation, and short-term profitability has created a continent of incrementalism (keep it the same – if not, we cannot deal with setbacks), where the fear of failure outweighs the ambition to create something new. The temptation to solve this problem through state-led industrial planning is a dangerous illusion that ignores the fundamental lessons of economic history.

If we are to unlock the next wave of human progress, we must abandon the comforting but false narrative of perfect competition and embrace the messy, unpredictable, and often monopolistic reality of innovation. This means creating an ecosystem that rewards bold bets and tolerates failure. It means light regulation, competitive taxation, and a culture that celebrates the entrepreneur, not the bureaucrat. The path to a better future is not paved with the good intentions of central planners but with the creative destruction of the free market. It is a path that leads, paradoxically, through the monopoly of progress.

In essence – we need the right balance. The EU has the most potential to maximize output by a minimal input! The US has to catch up on food safety and non capitalistic and predatory capitalism.

We all can learn something from each other – including not mentioned global super powers!

#Insight42 #PublicSectorInnovation #DigitalSovereignty #ZeroToOne #ThielDoctrine #GovTech #DigitalTransformation #GermanyDigital #EUTech #InnovationStrategy #PublicProcurement #SovereignTech #RegulatoryReform #CreativeDestruction #EconomicGrowth #DigitalDecade #SmartGovernment #PublicAdmin #TechPolicy #FutureOfGovernment

References

[1] Peter Thiel, “Competition is for Losers,” Wall Street Journal, September 12, 2014

[9] Federal Trade Commission, “FTC Sues Prescription Drug Middlemen for Artificially Inflating Insulin Drug Prices,” September 20, 2024

Related Topics:

https://insight42.com/unleash-the-european-bull/